Category: Taxes and Taxation

WTO panel rules against India

20, Apr 2023

Why in News?

- World Trade Organization (WTO) panel has ruled that India has violated global trading rules by imposing import duties on IT products, such as mobile phones and components, and integrated circuits.

What was the case?

- The case involved a dispute over India’s introduction of import duties ranging from 7.5% to 20% on a wide range of IT products, including mobile phones, components, and integrated circuits.

- The EU, Japan, and Taiwan challenged these import duties in 2019, arguing that they exceeded the maximum rate allowed under global trading rules.

- The recent ruling by the WTO panel found that India had violated these rules and recommended that India bring its measures into conformity with its obligations.

WTO Panel’s Ruling:

- The WTO panel has ruled that India violated global trading rules by imposing these import duties.

- The panel recommended that India bring these measures into conformity with its obligations.

- While the panel broadly backed the complaints against India, it rejected one of Japan’s claims that India’s customs notification lacked “predictability”.

Implications of the ruling:

- The EU is India’s third-largest trading partner, accounting for 10.8% of total Indian trade in 2021, according to the European Commission.

- The ruling could have implications for trade relations between India and the EU, as well as Japan and Taiwan.

- India may be required to lower or eliminate the challenged import duties.

- It remains to be seen whether India will appeal against the ruling.

- If it does, the case will sit in legal purgatory since the WTO’s top appeals bench is no longer functioning due to US opposition to judge appointments.

About the World Trade Organization:

- The WTO started functioning on 1 January 1995, but its trading system is half a century older. Since 1948, the General Agreement on Tariffs and Trade (GATT) had given the rules for the system. (The second WTO ministerial meeting, held in Geneva in May 1998, included a celebration of the 50th anniversary of the system.)

- It did not take long for the General Agreement to give birth to an unofficial, extant international organization, also known informally as GATT.

- Over the years, GATT evolved through several rounds of negotiations.

- The General Agreement on Tariffs and Trade (GATT) had its last round in 1986 and it lasted till 1994.

- This was known as the Uruguay Round and it led to the formulation of the World Trade Organization (WTO).

- While GATT mostly dealt with trade in goods, the WTO and its agreements could not only cover goods but also trade in services and other intellectual properties like trade creations, designs, and inventions.

- The WTO has 164 members and 23 observer governments. Afghanistan became the 164th member in July 2016. In addition to states, the European Union, and each EU country in its own right is a member.India is the original member of the World Trade Organization.

Purpose of WTO:

- To establish rule of law in international trade.

- To ensure free and fair trade.

- To maintain transparency and predictability in international trade.

- To contribute to the development of developing countries.

WTO and developing countries:

- The WTO classifies nations into developed, developing, and least developed countries (LDCs).

- The terms “developed” and “developing” countries are not defined by the WTO.

- The members declare themselves whether their countries are “developed” or “developing.”

- However, other members have the right to challenge the member’s choice to use a provision that is available to developing nations.

- Like IMF and World Bank where a system of weighted voting exists, in WTO also each country has an equal vote. WTO agreements require consensus.

- The Developing Country status comes with certain rights. The status ensures special and differentiating treatment (S&DT).

49th GST Council Meeting

22, Feb 2023

Why in News?

- Recently, the Goods and Services Tax (GST) Council in its 49th Meeting has reached consensus on the constitution of the GST Appellate Tribunal to resolve the rising number of disputes under the old indirect tax regime.

What are the Key Highlights of the GST Meeting?

- GST Appellate Tribunal:

- The council has approved the creation of a national tribunal mechanism with state benches for the redressal of disputes.

- The Tribunal will resolve the rising number of disputes under the GST regime that are now clogging High Courts and other judicial fora.

- This year’s Finance Bill can incorporate the enabling legislative provisions for the Tribunal.

- The GST Tribunal will have one principal bench in New Delhi and many benches or boards in states. The principal bench and state boards would have two technical and two judicial members each, with equal representation.

- But all four members would not sit to hear each case, which is likely to be decided based on the threshold or value of dues involved.

- Cleared Pending Compensation Dues:

- It has cleared the balance of Rs 16,982 crore (for June 2022).

- It has finalized GST compensation of Rs 16,524 crore to six states/UTs including, Delhi, Karnataka, Odisha, Puducherry, Tamil Nadu, and Telangana

- Lower Penal Charges:

- It approved lower penal charges for delayed filing of annual returns by businesses with a turnover of up to Rs 20 crore a year.

- The council has approved an Amnesty Scheme for taxpayers unable to file three statutory returns, that entail conditional waivers or reductions in late fees for such filings.

- The GST Amnesty Scheme was introduced to encourage non-filers to voluntarily come forward and file their GST returns by providing a one-time relief from late fees.

- Rate Changes:

- The GST rate on several items has been changed, such as pencil sharpeners, rab (liquid jaggery).

- The Council also decided to extend the GST exemption to educational institutions and central and state educational boards from conducting entrance examinations through any authority, including the National Testing Agency.

- Plugging Tax Evasion:

- The Council has decided to switch the compensation cess levied on pan masala and gutkha commodities from an ad valorem basis to a specific tax-based levy.

- The ad valorem tax is levied according to value.

- This will boost the first stage collection of the revenue.

- The Council also mandated that exports only be allowed against letters of undertaking assuring of GST compliance.

What is the GST Council?

- It is a joint forum of the Centre and the states.

- It was set up by the President as per Article 279A (1) of the amended Constitution.

- The members of the Council include the Union Finance Minister (chairperson), the Union Minister of State (Finance) from the Centre.

- Each state can nominate a minister in-charge of finance or taxation or any other minister as a member.

- According to Article 279 of the Constitution, the council can make recommendations to the Union and the states on important issues related to GST, like the goods and services that may be subjected or exempted from GST, model GST Laws”.

- Article 279 as well as Article 279A of the Indian Constitution deal with the financial provisions of the country.

- They are specifically related to the calculation of “net proceeds” from Union duties and taxes on goods and the formation of the Goods and Services Tax Council, respectively.

- It also decides on various rate slabs of GST.

- For instance, an interim report by a panel of ministers has suggested imposing 28 % GST on casinos, online gaming and horse racing.

What is Goods and Services Tax?

- GST was introduced through the 101st Constitution Amendment Act, 2016.

- It is one of the biggest indirect tax reforms in the country.

- It was introduced with the slogan of ‘One Nation One Tax’.

- The GST has subsumed indirect taxes like excise duty, Value Added Tax (VAT), service tax, luxury tax etc.

- It is essentially a consumption tax and is levied at the final consumption point.

- This has helped mitigate the double taxation, cascading effect of taxes, multiplicity of taxes, classification issues etc., and has led to a common national market.

- The GST that a merchant pays to procure goods or services (i.e. on inputs) can be set off later against the tax applicable on supply of final goods and services.

- The set off tax is called input tax credit.

- The GST avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

Tax Structure under GST:

- Central GST to cover Excise duty, Service tax etc,

- State GST to cover VAT, luxury tax etc.

- Integrated GST (IGST) to cover inter-state trade.

- IGST per se is not a tax but a system to coordinate state and union taxes.

- It has a 4-tier tax structure for all goods and services under the slabs- 5%, 12%, 18% and 28%.

What are the Issues Related to GST?

Complexity:

- The GST system in India is quite complex, with multiple tax rates, exemptions, and compliance requirements.

- It hampers the progress of a single indirect tax rate for all the goods and services in the country.

High Tax Rates:

- Some industries and goods are subject to high GST rates, which can make them unaffordable for many consumers.

- For example, the tax rate on luxury goods and services is 28%, which is quite high.

- Though rates are rationalized, 50% of items are under the 18% bracket.

Compliance Burden:

- The GST regime has a lot of compliance requirements, including filing of returns, maintaining records, and regular audits. This can be a burden for businesses, especially small and medium enterprises.

Technical Issues:

- There have been reports of technical glitches in the GST network, leading to delays in filing returns and claiming input tax credits.

Impact on the Unorganized Sector:

- The unorganized sector, which forms a significant part of the Indian economy, has been adversely affected by the GST.

- Many small businesses and traders have found it challenging to comply with the new tax regime.

Lack of Clarity:

- There is still a lack of clarity on some aspects of the GST regime, such as the classification of goods and services and the applicability of tax rates. This lack of clarity can create confusion and disputes.

Way Forward:

- Simplifying the compliance process, providing easier access to information, and increasing support for taxpayers can help address this issue.

- Technical issues such as system downtimes, portal errors, and other glitches can cause significant disruptions for businesses. Addressing these technical issues can help businesses comply with GST requirements more effectively.

- Many small businesses and traders are not fully aware of the GST system and its implications. Increasing awareness and education about the GST system can help improve compliance and reduce errors.

- GST is a collaborative effort between the central and state governments, and coordination between them is crucial to its success. Improving communication and coordination can help ensure a smooth implementation of the GST system.

GST revenues rise 15% in December 2022, says Finance Ministry

02, Jan 2023

Why in News?

- India’s Goods and Services Tax (GST) revenues rose to nearly ₹1.5 lakh crore in December 2022, 15% higher than a year ago and 2.5% over November’s collections that had marked a three-month low.

About the News:

- This is the tenth month in a row that GST collections have crossed the ₹1.4 lakh crore mark, with revenues from import of goods rising 8% and revenues from domestic transactions (including import of services) up 18% from the revenues yielded by these sources during December 2021.

- The gross GST revenue collected during December 2022, which reflect transactions undertaken in November, is ₹1,49,507 crore, of which Central GST (CGST) is ₹26,711 crore, State GST (SGST) is ₹33,357 crore, Integrated GST (IGST) is ₹78,434 crore (including ₹40,263 crore collected on import of goods) and Cess is ₹11,005 crore (including ₹850 crore collected on import of goods), the Finance Ministry said.

- “The Government has settled ₹36,669 crore to the CGST and ₹31,094 crore to SGST from IGST as regular settlement. The total revenue of Centre and the States after regular settlements in the month of December 2022 is ₹63,380 crore for CGST and ₹64,451 crore for the SGST,” it added.

- On a sequential basis, while there was a 2.5% rise in revenues from November to December 2022, the number of e-way bills generated went up 3.95% to 7.9 crore in December.

- While revenues from domestic transactions rose 18% overall, a dozen States recorded higher growth in tax collections and 13 States reported slower growth rates.

- Goa, Odisha and Manipur reported a contraction in revenues of 22%, 6% and 5%, respectively, even as Chhatisgarh’s revenues were flat year-on-year.

- Bihar reported the highest growth in revenues at 36%, followed by Nagaland (30%), the erstwhile State of Jammu and Kashmir (28%), Arunachal Pradesh (27%), with Gujarat and Andhra Pradesh seeing GST inflows rise by 26% each. Tamil Nadu’s revenues rose 25%, followed closely by Rajasthan and West Bengal (24%), Madhya Pradesh (22%) and Maharashtra (20%).

- Among the Union Territories, Ladakh reported a sharp 68% spike in revenues, followed by Dadra Nagar Haveli (37%), Chandigarh (33%) and Puducherry (30%). However, Daman and Diu reported a whopping 86% drop in GST collections, with Lakshadweep and Andaman and Nicobar Islands also recording contractions of 36% and 19%, respectively.

- Abhishek Jain, partner indirect tax, KPMG said the robust GST collections suggest that ₹1.5 lakh crore may be ‘the new normal’ for monthly revenues, as the December’s numbers came in after peak festive sales are over.

What are the reasons for the Rise of the GST?

- The sharp surge has come on the back of anti-evasion measures, “especially action against fake billers”, and a pick-up in economic activity.

- Rate rationalization measures undertaken by the GST Council to correct ‘inverted duty structure’.

- Inverted Tax Structure refers to a situation where the rate of tax, that is GST, on inputs is higher than the rate of tax on output supplies or finished goods.

- Economic recovery and increased domestic consumption.

- The total number of e-way bills generated in February was 6.91 crore, higher than 6.88 crore seen a month ago, despite it being a shorter month, which indicates the “recovery of business activity at faster pace”.

What is Goods and Services Tax?

- GST was introduced through the 101st Constitution Amendment Act, 2016.

- It is one of the biggest indirect tax reforms in the country.

- It was introduced with the slogan of ‘One Nation One Tax’.

- The GST has subsumed indirect taxes like excise duty, Value Added Tax (VAT), service tax, luxury tax etc.

- It is essentially a consumption tax and is levied at the final consumption point.

- This has helped mitigate the double taxation, cascading effect of taxes, multiplicity of taxes, classification issues etc., and has led to a common national market.

- The GST that a merchant pays to procure goods or services (i.e. on inputs) can be set off later against the tax applicable on supply of final goods and services.

- The set off tax is called input tax credit.

- The GST avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

Tax Structure under GST:

- Central GST to cover Excise duty, Service tax etc,

- State GST to cover VAT, luxury tax etc.

- Integrated GST (IGST) to cover inter-state trade.

- IGST per se is not a tax but a system to coordinate state and union taxes.

- It has a 4-tier tax structure for all goods and services under the slabs- 5%, 12%, 18% and 28%.

Decriminalisation of offences under GST

21, Dec 2022

Why in News?

- The Finance Minister chaired the 48th GST Council, which recommended decriminalising certain offences under Section 132 of the Central Goods and Services Tax (CGST) Act, 2017

What is the issue?

- The GST law is still in its early stages of development. Hence, it is vital to recognise that imposing penal provisions in an uncertain ecosystem impacts an enterprise’s ability to conduct business.

What is Goods and Services Tax?

- GST was introduced through the 101st Constitution Amendment Act, 2016.

- It is one of the biggest indirect tax reforms in the country.

- It was introduced with the slogan of ‘One Nation One Tax’.

- The GST has subsumed indirect taxes like excise duty, Value Added Tax (VAT), service tax, luxury tax etc.

- It is essentially a consumption tax and is levied at the final consumption point.

- This has helped mitigate the double taxation, cascading effect of taxes, multiplicity of taxes, classification issues etc., and has led to a common national market.

- The GST that a merchant pays to procure goods or services (i.e. on inputs) can be set off later against the tax applicable on supply of final goods and services.

- The set off tax is called input tax credit.

- The GST avoids the cascading effect or tax on tax which increases the tax burden on the end consumer.

Offences under GST:

- Despite technology leverage, instances of tax evasion have surged due to culprits remaining undetected.

- The GST law imposes severe penalties and guidelines in order to combat corruption and maintain an efficient tax collection system.

Penalties under GST law:

- The department authorities have the jurisdiction to impose monetary fines and the seizure of goods as penalties for violating statutory provisions.

- Criminal penalties include imprisonment and fines but can be awarded only in a criminal court following a prosecution.

- The amount of tax evaded, the amount of Input Tax Credit (ITC) improperly claimed or used, etc, determines the length of the prison sentence.

- The Act also divides offences into – cognisable and bailable and non-cognisable and bailable.

Measures recommended at the 48th GST Council meeting:

- Raising the minimum tax amount for commencing a GST prosecution from one to two crore.

- Reducing the compounding amount from 50 to 150% of the tax amount to 25 to 100% of the tax amount.

- Decriminalising certain offences under Section 132 of the CGST Act, 2017, such as preventing an officer from doing his duties, deliberate tampering with material evidence and failure to supply information.

- Other suggestions include refunding unregistered individuals and facilitating e-commerce for small businesses.

What impact will the aforementioned measures have?

- Prosecution, arrest, and imprisonment in GST cases would occur only in the most exceptional cases.

- Ease of doing business will be made more effective.

Extending the GST Compensation

07, Jan 2022

Why in News?

- Finance Ministers of several States have demanded that the GST compensation scheme be Extended beyond June 2022.

What’s the Issue?

- The adoption of GST was made possible by States ceding almost all their powers to impose local-level indirect taxes and Agreeing to let the prevailing multiplicity of imposts be Subsumed into the GST.

- This was agreed on the condition that revenue shortfalls arising from the transition to the new indirect taxes regime would be made good from a pooled GST Compensation Fund for a period of five Years that is set to end in June 2022.

Need for Extension:

- Citing the impact of the COVID-19 pandemic on the overall economy and more specifically States’ revenues, the States including Tamil Nadu, Kerala, West Bengal, Rajasthan and Chhattisgarh stressed that while their revenues had been adversely impacted by the introduction of GST, the hit from the pandemic had pushed back any possible rebound in revenue especially at a time when they had been forced to spend substantially more to address the public health emergency and its socio-economic fallout on their residents.

What is the GST Compensation?

- The Constitution (One Hundred and First Amendment) Act, 2016, was the law which created the mechanism for levying a common nationwide Goods and Services Tax (GST).

- While States would receive the SGST (State GST) component of the GST, and a share of the IGST (integrated GST), it was agreed that revenue shortfalls arising from the transition to the new indirect taxes regime would be made good from a pooled GST Compensation Fund for a period of five years that is currently set to end in June 2022.

How is the GST Compensation Fund funded?

- This corpus is funded through a Compensation cess that is levied on so-called ‘demerit’ Goods.

- The items are pan masala, Cigarettes and tobacco products, aerated water, caffeinated Beverages, Coal and certain Passenger motor vehicles.

Computation of the Shortfall:

- The computation of the shortfall is done annually by projecting a revenue assumption based on 14% compounded growth from the base year’s (2015-2016) revenue and calculating the difference between that figure and the actual GST collections in that year.

Can the deadline be Extended? If so, how?

- The deadline for GST compensation was set in the original legislation and so in order to extend it, the GST Council must first recommend it and the Union government must then move an amendment to the GST law allowing for a new date beyond the June 2022 deadline at which the GST compensation scheme will come to a close.

Anti-Dumping Duty on Five Chinese Goods

29, Dec 2021

Why in News?

- India has imposed anti-dumping duty on five Chinese products, including certain Aluminium Goods and some Chemicals, for Five Years to guard local manufacturers from cheap imports from the Neighbouring Country.

About the News:

- According to Separate Notifications of the Central Board of Indirect Taxes and Customs (CBIC), the duties have been imposed on certain flat rolled products of aluminium; sodium hydrosulphite (used in dye industry); silicone sealant (used in manufacturing of solar photovoltaic modules, and thermal power applications); hydrofluorocarbon (HFC) component R-32; and Hydrofluorocarbon blends (both have uses in refrigeration industry).

- These duties were imposed following recommendations of the Commerce Ministry’s investigation arm, the Directorate General of Trade Remedies (DGTR).

- The DGTR, in separate probes, has concluded that these products have been exported at a price below normal value in Indian markets, which has resulted in Dumping and has suffered material injury due to the dumping.

- India’s exports to China during the April-September 2021 period were worth $12.26 billion while imports aggregated at $42.33 billion, leaving a trade deficit of $30.07 billion.

What is Dumping?

- In international trade practise, dumping happens when a country or a firm exports an item at a price lower than the price of that product in its domestic market.

- Dumping impacts the price of that product in the importing country, hitting margins and profits of local Manufacturing Firms.

What is Anti-Dumping Duty?

- Anti-dumping duty is imposed to rectify the situation arising out of the dumping of goods and its Trade Distortive Effect.

- According to Global Trade norms, including the World Trade Organization (WTO) regime, a country is allowed to impose tariffs on such dumped products to provide a level-playing field to Domestic Manufacturers.

- The duty is aimed at ensuring fair trading practices and creating a level-playing field for domestic producers vis-a-vis foreign producers and exporters.

- While the DGTR recommends the duty to be levied, the Finance Ministry imposes it.

How is it Different from CVD?

- Anti-dumping duty is different from countervailing duty. The latter is imposed in order to counter the negative impact of import subsidies to protect domestic producers.

- Countervailing Duties (CVDs) are tariffs levied on imported goods to offset subsidies made to producers of these goods in the exporting country.

- CVDs are meant to level the playing field between domestic producers of a product and foreign producers of the same product who can afford to sell it at a lower price because of the subsidy they receive from their Government.

LIQUOR REVENUE FOR STATES

06, May 2020

Why in News?

- Recently, the central government eased restrictions in the third phase of the nationwide lockdown and allowed the sale of liquor.

About the News:

- The Delhi government announced a 70% hike as ‘Special Corona Fee’ in the price of liquor across categories. This shows the importance of liquor to the economy of the states.

- Liquor contributes a considerable amount to the exchequers of all states and Union Territories (UTs) except Gujarat and Bihar, both of which have enforced prohibition.

- Andhra Pradesh announced prohibition in 2019, however, sale of the liquor has been allowed with “prohibition tax”.

- States levy excise duty on manufacture and sale of liquor.

- States also charge special fees on imported foreign liquor, transport fee, and label & brand registration charges.

- A few states like Uttar Pradesh, have imposed a ‘special duty on liquor’ to collect funds for special purposes, such as maintenance of stray cattle.

RBI’s report on State Finance:

- The Reserve Bank of India published the report ‘State Finances: A Study of Budgets of 2019-20’ in September 2019.

- It shows that state excise duty on alcohol accounts for around 10-15% of Own Tax Revenue of a majority of states.

- In fact, state excise duties on liquor is the second or third largest contributor to the category State’s Own Tax revenue; Goods and Services Tax-GST is the largest.

- This is the reason states have always wanted liquor kept out of the purview of GST.

- According to the report, in 2019-20, state GST had the highest share, 43.5%, in states’ Own Tax Revenue, followed by Sale Tax at 23.5% (mainly on petroleum products which are out of GST), state excise at 12.5%, and taxes on property and capital transactions at 11.3%.

About State Excise:

- Excise duty on production of few items including that on liquor and other alcohol-based items is imposed and collected by state governments and is called ‘State Excise’ duty.

- Excise duty is basically a production tax. It is imposed on manufactured items in India that are meant for domestic consumption.Revenue receipts from state excise come mainly from commodities such as Country Spirits; Liquor; Foreign Liquors and Spirits; Medicinal and Toilet Preparations containing Alcohol, Opium etc; Opium, Hemp and other Drugs; Sales to Canteen Stores Depots. Apart from these, a substantial amount comes from licences, fine and confiscation of alcohol products.

What are the Sources of Revenue for States?

Tax Revenue:

- State’s Own Tax Revenue:

- Taxes on Income (agricultural income tax and taxes on professions, trades, callings and employment)

- Taxes on Property and Capital Transactions (land revenue, stamps and registration fees, urban immovable property tax)

- Taxes on Commodities and Services (sales tax, state sales tax/VAT, central sales tax, surcharge on sales tax, receipts of turnover tax, other receipts, state excise, taxes on vehicles, taxes on goods and passengers, taxes and duties on electricity, entertainment tax, state GST, and “other taxes and duties”)

Share in Central Taxes:

- Article 280 of the Indian Constitution requires the composition of the Finance Commission in every five years so that the states can get a reasonable part in the tax revenue of the Union Government.

Non-Tax Revenue:

- These are collected by the governments for providing/facilitating any goods and service.

- It is compulsory to pay a part of the income earned/generated and amount of goods and services consumed as tax. However, non-tax revenue becomes payable only when services offered by the government are availed.

Other Components:

- Interest:It comprises interest of loans given to states and union territories for reasons like non-plan schemes and planned schemes with a maturity period of 20 years and also interest on loans advanced to Public Sector Enterprises (PSEs), Port Trusts and other statutory bodies etc.

- Dividends and profits, Petroleum license, Power supply fees, Fees for Communication Services, Broadcasting fees, Road, Bridges usage fees, Examination fees etc.

RAJYA SABHA NOD FOR VIVAD SE VISHWAS BILL

14, Mar 2020

Why in News?

- Recently, the Parliament has passed an amendment to the ‘Direct Tax Vivad se Vishwas Bill, 2020’ in order to widen its scope to cover litigation pending in various Debt Recovery Tribunals (DRTs).

About the Amendment:

- The amendment also includes certain search and seizure cases where the recovery is up to Rs. 5 crore.

- Therefore, the Bill in current form allows taxpayers to settle cases pending before the Commissioner (Appeals), Income Tax Appellate Tribunals (ITATs), Debt Recovery Tribunals (DRTs), High Courts and the Supreme Court.

- The Direct Tax Vivad se Vishwas Bill, 2020 is similar to the ‘Sabka Vishwas Scheme’, which was brought in to reduce litigation in indirect taxes in the year 2019. It resulted in settling over 1, 89,000 cases.

- Under the Sabka Vishwas Scheme, the government expected to raise around 39,500 crore. However, after the closure of the amnesty window in January 2020 application in relation to taxes worth Rs. 90,000 crore were received. This shows the success of the scheme.

What are its Key Features?

- Objective: The Bill provides a mechanism for resolution of pending tax disputes related to direct taxes (Income Tax and Corporate Tax)in simple and speedy manner.

- Reduce Litigation: According to the Finance Ministry, at present there are 4.83 lakh pending direct tax cases worth Rs.9 lakh crore in the courts. Through this scheme, the government wants to recover this money in a swift and simple way

- Addressing Revenue Shortfall: The government is witnessing a big shortfall in revenues, especially tax revenues, hence, increasing revenues in one of the priorities of the Government.

- Direct Tax collections have been lower than their budget targets due to the overall economic slowdown and a cut in the corporate tax rate in September, 2019.

- Mechanism: In case of payment of tax, a taxpayer would be required to pay only the amount of the disputed taxes and will get complete waiver of interest, penalty and prosecution provided he/she pays by March 31, 2020.

- But, if the tax arrears relate to disputed interest or penalty only, then 25% of disputed penalty or interest will have to be paid.

- Those who avail this scheme after March 31, 2020 will have to pay some additional 10% amount. However, the scheme will remain open till June 30, 2020.

- Immunity to Appellant: Once a dispute is resolved, the designated authority cannot levy interest or penalty in relation to that dispute.

- Further, no appellate forum can make a decision in relation to the matter of dispute once it is resolved.

- Revival of Disputes: However, if an appellant provides false information or violates the Income Tax Act, 1961, then case of dispute can be revived.

Other Issues Related to the Bill:

- Few MP’s also raised concern about the Hindi name of the bill, which claimed to be a violation of Article 348.

- Article 348 talks about the Language to be used in the Supreme Court and in the High Courts and for Acts, Bills, etc.

- Notwithstanding anything in the foregoing provisions of this Part, until Parliament by law otherwise provides

- all proceedings in the Supreme Court and in every High Court,

- the authoritative texts

- of all Bills to be introduced or amendments thereto to be moved in either House of Parliament or in the House or either House of the Legislature of a State,

- of all Acts passed by Parliament or the Legislature of a State and of all Ordinances promulgated by the President or the Governor of a State, and

- of all orders, rules, regulations and bye laws issued under this Constitution or under any law made by Parliament or the Legislature of a State, shall be in the English language.

DIRECT TAX VIVAD SE VISHWAS BILL, 2020

17, Feb 2020

Why in News?

- The Union Cabinet has recently approved an amendment to the ‘Direct Tax Vivad se Vishwas Bill, 2020’ in order to widen its scope to cover litigation pending in various Debt Recovery Tribunals (DRTs).

Key provisions of the Bill:

Mechanism:

- The Bill provides a mechanism for resolution of pending tax disputes related to direct taxes (Income Tax and Corporate Tax) in simple and speedy manner.

- The Bill in current form allows taxpayers to settle cases pending before the Commissioner (Appeals), Income Tax Appellate Tribunals (ITATs), Debt Recovery Tribunals (DRTs), High Courts and the Supreme Court.

- Under the proposed Vivad Se Vishwas scheme, a taxpayer would be required to pay only the amount of the disputed taxes and will get complete waiver of interest and penalty provided he pays by March 31, 2020.

- But, if the tax arrears relate to disputed interest or penalty only, then 25% of disputed penalty or interest will have to be paid.

- Those who avail this scheme after March 31, 2020 will have to pay some additional amount.

- However, the scheme will remain open only till June 30, 2020. Those who avail this scheme after March 31, 2020 will have to pay some additional amount.

- The scheme also applies to all case appeals that are pending at any level.

- The recent amendment also includes certain search and seizure cases where the recovery is up to ₹5 crore.

Immunity to Appellant:

- Once a dispute is resolved, the designated authority cannot levy interest or penalty in relation to that dispute.

- Further, no appellate forum can make a decision in relation to the matter of dispute once it is resolved.

Revival of Disputes:

- However, if an appellant provides false information or violates the Income Tax Act, 1961, then case of dispute can be revived.

Significance of the Bill:

1. Reduce Litigation:

- According to the Finance Ministry, at present there are 4.83 lakh pending direct tax cases worth Rs.9 lakh crore in the courts. Through this scheme, the government wants to recover this money in a swift and simple way.

2. Addressing Revenue Shortfall:

- The government is witnessing a big shortfall in revenues, especially tax revenues, hence, increasing revenues in one of the priorities of the government.

- Direct Tax collections have been lower than their budget targets due to the overall economic slowdown and a recent cut in the corporate tax rate.

Similar Schemes:

- The Direct Tax Vivad se Vishwas Bill, 2020 is similar to the ‘Sabka Vishwas Scheme’, which was brought in to reduce litigation in indirect taxes in the year 2019. It resulted in settling over 1,89,000 cases.

- {“Vivad se Vishwas Scheme” will be for the direct tax related disputes whereas “Sabka Vishwas” is for Indirect Tax Related Disputes.}

PURIFIED TEREPHTHALIC ACID (PTA)-ABOLISHED

06, Feb 2020

Context:

- Recently, the government has abolished anti-dumping duty on a chemical called Purified Terephthalic Acid (PTA).

- It was also being mentioned by the Finance Minister in her Budget speech.

About Purified Terephthalic Acid (PTA):

- It is important for those who are in the manufacturing sector of man-made fabrics or their component – makes up for around 70-80% of a polyester product.

- It is a crucial raw material used to manufacture polyester coatings resins for use in the formulation of general metal, appliance, automotive, industrial maintenance, and coil coatings.

- What is Dumping? It is said to occur when the goods are exported by a country to another country at a price lower than the price it normally charges in its own home market. This is an unfair trade practice which can have a distortive effect on international trade.

- What is Anti-dumping? It is a measure to rectify the situation arising out of the dumping of goods and its trade distortive effect.

- Anti-dumping duty is used as an instrument of fair competition which is permitted by the World Trade Organisation (WTO).

Reason for the Controversy:

- The domestic companies facing with limited domestic suppliers of PTA because of their costlier product less attractive for their domestic and international buyers.

- An increase in imports of the products they had been producing, as there was no safeguard against imports of cheaper versions of these downstream polyester-based products.

- The abolition of Anti-Dumping Duty on PTA has come after persistent demand from the manufacturing and Textile Industry.

- Other raw materials: Mono Ethylene Glycol (MEG), another raw material used in the manufacturing of polyester, is currently the subject of another anti-dumping duty investigation initiated by DGTR recently.

Directorate General of Trade Remedies:

- The anti-dumping duty on PTA was imposed after domestic manufacturers approached the Directorate General of Trade Remedies (DGTR).

- It is the apex national authority under the Ministry of Commerce and Industry.

- It administers all trade remedial measures including anti-dumping, countervailing duties and safeguard measures.

- It provides trade defence support to the domestic industry and exporters in dealing with increasing instances of trade remedy investigations instituted against them by other countries.

TAX RELIEF FOR FOOD AT INCORPORATED CLUBS

07, Oct 2019

Why in News?

- In a significant judgment, the Supreme Court has held that supply of food, drinks and beverages by an incorporated members’ club to its permanent members is not liable for sales or service tax.

Issue:

- The Bench was answering a reference on the question of whether the doctrine of mutuality highlighted in the Young Men’s Indian Association judgment of the Constitution Bench would survive the 46th Constitutional Amendment, which introduced Article 366 (29-A) into the Constitution.

- The particular Article dealt with the taxation of sale of goods. Its clauses said that the supply or service of ‘goods’ like food or drink by an “unincorporated association or body of persons’ would be taxable.

Highlights:

- The Supreme Court has ruled that the doctrine of mutuality continues to be applicable to incorporated and unincorporated members’ clubs.

- The doctrine of mutuality, based on common law principles, is premised on the theory that a person cannot make a profit from himself.

- An amount received from oneself, therefore, cannot be regarded as income and is not taxable.

- Thus, Sales Tax cannot be levied on Clubs, whether incorporated or unincorporated for the supply of food and drinks to permanent members.

- The Court said such supply of goods lacks the essential aspect of a sale — a seller and a buyer.It was said that the legal entity called the club and its members are one and the same. The club, though a distinct legal entity, is only an agent of its members.

- The Supreme Court has held that, in the case of sales tax, both incorporated and un-incorporated members’ clubs are exempt from liability of paying sales tax.

- The Bench referred to the Constitution Bench judgment in the Young Men’s Indian Association case and held that the doctrine of mutuality between the club and its members would dominate the relationship between an incorporated members’ club and its permanent members.

- The rendering of service by the petitioner-club to its members is not taxable service under the Finance Act, 1994, the court held.

A DEEP CUT IN THE CORPORATE TAXES

23, Sep 2019

Context:

- In order to revive the economy from the economic slowdown, the Finance Minister has announced a slew of major changes in corporate income tax rates. This has been made through an ordinance – the Taxation Laws (Amendment) Ordinance 2019 that amends Income Tax Act of 1961 and the Finance Act of 2019.

Key provisions of the ordinance:

- The central government slashed corporate tax rates for domestic firms from 30% to 22% and for new manufacturing companies from 25% to 15% to boost economic growth.

- Effective corporate tax rate after surcharge and cess on this companies would be 25.17 percent. No Minimum Alternate Tax (MAT) applicable on such companies.

- Local companies incorporated after October 2019 and till March 2023, will pay tax at 15 percent.

- That effective tax for new companies shall be 17.01 percent, including cess and surcharge.

- Companies enjoying tax holidays would be able to avail concessional rates post the exemption period.

- MAT relief for those companies opting to continue paying surcharge and cess. MAT has been reduced to 15 percent from 18.5 percent for companies who continue to avail exemptions and incentives.

- Enhanced surcharge announced in Budget 2019 will not apply on capital gains arising on sale of any security, including derivatives by foreign portfolio investors (FPI).

Pros associated with the above move:

- Lower taxes will result in higher profit margins. This will bolster their books, and some of these companies should be able to pass on the higher margins in the form of lower product prices to consumers.

- Lower corporate income tax rates and the resultant increase in profitability of the company will definitely prompt companies to invest more, raising their capital expenditure (capex).

- Increase in the capacities of the company will eventually result in the increased employment opportunities for the youngsters.

- Given the substantially lower rates would imply that many corporates will break even much ahead than what would have been the case with the earlier rates.

- The ultimate goal of turning India into investors’ darling, demonstrating the government’s intent to walk the talk on economic management, restoring investors’ confidence and boosting sentiments and demand will be definitely meet its success point.

- It is expected that it will give a great stimulus to ‘Make in India’, attract private investment from across the globe, improve the competitiveness of the private sector, create more jobs.

- The reduction in corporate tax, effectively, brings India’s ‘headline’ corporate tax rate broadly at par with an average of 23% rate in Asian countries.

Impacts of the Rate Cut:

- The latest corporate income tax will result in the revenue foregone to the tune of Rs 1.45 lakh crore a year to the government.

- The government has set a fiscal deficit target of 3.3 percent of GDP for 2019-20. So the latest move has raised concerns of fiscal slippage, given that tax collections have been far below the budgeted estimates.

Corporate tax – A Global Scenario

- The new corporate income tax rates in India will be comparatively lower than USA (27 percent), Japan (30.62 percent), Brazil (34 percent), Germany (30 percent) and is similar to China (25 percent) and Korea (25 percent).

- Effective tax rate of 17 percent on newly incorporated companies in India with is almost equivalent to what corporates pay in Singapore (17 percent).

What is Revenue Foregone?

- Foregone earnings are the difference between earnings actually achieved and earnings that could have been achieved with the absence of specific fees, expenses or lost time.

37TH GST COUNCIL MEETING

21, Sep 2019

Why in News?

- The 37th GST Council met on 20th September 2019 in Goa under the chairmanship of Union Finance Minister.

Key Recommendations:

- Relaxations in annual returns filing for MSMEs for the financial year 2017 – 18 and 2018 – 19.

- A committee of officers would be appointed for examining the simplification of forms for annual return and reconciliation statement.

- Extension of the last date for filing of appeals against orders of the Appellate Authority before the GST Appellate Tribunal as the Appellate Tribunals are yet not functional.

- The new return system would be introduced from April 2020 instead of the previously proposed October 2019.

- Suitable amendments would be made to the CGST Act, UTGST Act and corresponding SGST Acts in view of the creation of the union territories of Jammu & Kashmir and Ladakh.Integrated refund system with disbursal by a single authority to be introduced from 24th September 2019.

- The Council also took an in-principle decision to link Aadhaar with the registration of taxpayers under GST and also to examine the possibility of making the 12-digit unique identification number mandatory for claiming refunds.

- Changes were also made to the GST rates for various goods and services.

GST Council:

- The Goods and Services Tax Council is a constitutional body for making recommendations to the Union and State Governments on issues related to Goods and Service Tax.

- It is chaired by the Union Finance Minister.

- The other members are the Union State Minister of Revenue or Finance, and Ministers in-charge of Finance or Taxation of all the States.

CBDT ENTERS INTO 26 APAS

05, Sep 2019

Why in News?

- The Central Board of Direct Taxes (CBDT) has entered into 26 Advance Pricing Agreements (APAs) in the first 5 months of the financial year (April to August, 2019).

- Out of these 26 APAs, 1 is a BAPA entered into with the United Kingdom and the remaining 25 are Unilateral Advance Pricing Agreements (UAPAs).

APA:

- An advance pricing agreement (APA) is an ahead-of-time agreement between a taxpayer and a tax authority on an appropriate transfer pricing methodology (TPM) for a set of transactions at issue over a fixed period of time.

Bilateral and Multilateral APAs:

- Bilateral APAs (BAPA) are those that also include agreements between the taxpayer and one or more foreign tax administrations under the authority of the mutual agreement procedure (MAP) specified in Income Tax Treaties.

- The taxpayer benefits from such agreements since they are assured that income associated with covered transactions is not subject to Double Taxation.

Significance:

- The progress of the APA scheme strengthens the Government’s resolve of fostering a non-adversarial tax regime.

- The Indian APA programme has been appreciated nationally and internationally for being able to address complex transfer pricing issues in a fair and transparent manner.

GOODS & SERVICES TAX

03, Jul 2019

Why in News?

- 2nd anniversary of Goods & Services Tax to be celebrated on 1st July 2019.

GST:

- GST is one indirect tax for the whole nation, which will make India one unified common market.

- GST is a single tax on the supply of goods and services, right from the manufacturer to the consumer.

- Credits of input taxes paid at each stage will be available in the subsequent stage of value addition, which makes GST essentially a tax only on value addition at each stage.

- The final consumer will thus bear only the GST charged by the last dealer in the supply chain, with set-off benefits at all the previous stages.

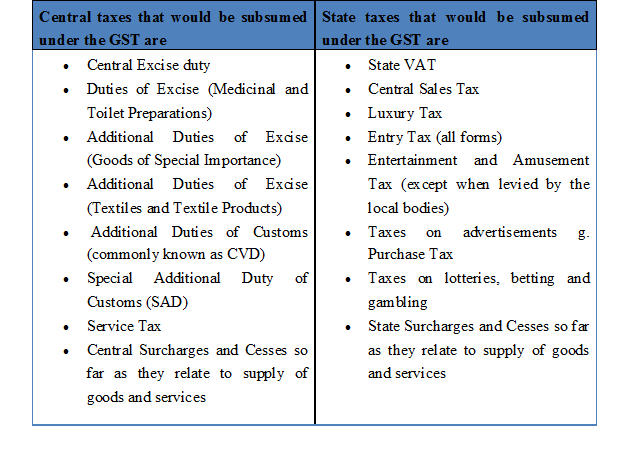

Taxes at the Centre and State level are subsumed into GST:

- At the Central level, the following taxes are being subsumed:

- Central Excise Duty

- Additional Excise Duty

- Service Tax

- Additional Customs Duty commonly known as Countervailing Duty, and

Special Additional Duty of Customs. - At the State level, the following taxes are being subsumed:

- Subsuming of State Value Added Tax/Sales Tax,

- Entertainment Tax (other than the tax levied by the local bodies), Central Sales

- Tax (levied by the Centre and collected by the States),

- Octroi and Entry tax,

- Purchase Tax,

- Luxury tax, and

- Taxes on lottery, betting and gambling.

Benefits of GST:

For business and industry:

- Easy compliance: A robust and comprehensive IT system would be the foundation of the GST regime in India. Therefore, all tax payer services such as registrations, returns, payments, etc. would be available to the taxpayers online, which would make compliance easy and transparent.

- Uniformity of Tax Rates and Structures: GST will ensure that indirect tax rates and structures are common across the country, thereby increasing certainty and ease of doing business. In other words, GST would make doing business in the country tax neutral, irrespective of the choice of place of doing business.

- Removal of cascading: A system of seamless tax-credits throughout the value-chain, and across boundaries of States, would ensure that there is minimal cascading of taxes. This would reduce hidden costs of doing business.

- Improved competitiveness: Reduction in transaction costs of doing business would eventually lead to an improved competitiveness for the trade and industry.

- Gain to manufacturers and exporters: The subsuming of major Central and State taxes in GST, complete and comprehensive set-off of input goods and services and phasing out of Central Sales Tax (CST) would reduce the cost of locally manufactured goods and services. This will increase the competitiveness of Indian goods and services in the international market and give boost to Indian exports. The uniformity in tax rates and procedures across the country will also go a long way in reducing the compliance cost.

For Central and State Governments:

- Simple and easy to administer: Multiple indirect taxes at the Central and State levels are being replaced by GST. Backed with a robust end-to-end IT system, GST would be simpler and easier to administer than all other indirect taxes of the Centre and State levied so far.

- Better controls on leakage: GST will result in better tax compliance due to a robust IT infrastructure. Due to the seamless transfer of input tax credit from one stage to another in the chain of value addition, there is an in-built mechanism in the design of GST that would incentivize tax compliance by traders.

- Higher revenue efficiency: GST is expected to decrease the cost of collection of tax revenues of the Government, and will therefore, lead to higher revenue efficiency.

For the consumer:

- Single and transparent tax proportionate to the value of goods and services: Due to multiple indirect taxes being levied by the Centre and State, with incomplete or no input tax credits available at progressive stages of value addition, the cost of most goods and services in the country today are laden with many hidden taxes. Under GST, there would be only one tax from the manufacturer to the consumer, leading to transparency of taxes paid to the final consumer.

- Relief in overall tax burden: Because of efficiency gains and prevention of leakages, the overall tax burden on most commodities will come down, which will benefit consumers.

GST Council:

- As per Article 279A (4), the Council will make recommendations to the Union and the States on important issues related to GST, like the goods and services that may be subjected or exempted from GST, model GST Laws, principles that govern Place of Supply, threshold limits, GST rates including the floor rates with bands, special rates for raising additional resources during natural calamities/disasters, special provisions for certain States, etc.

- As per Article 279A of the amended Constitution, the GST Council will be a joint forum of the Centre and the States. This Council shall consist of the following members namely: –

- Union Finance Minister.. Chairperson

- The Union Minister of State, in-charge of Revenue of finance… Member

- The Minister In-charge of finance or taxation or any other Minister nominated by each State Government.

CENTRE RATIFIES INTERNATIONAL CONVENTION TO CURB COMPANY PROFIT SHIFTING

03, Jul 2019

- Context: India has recently ratified the international agreement to curb Base Erosion and Profit Shifting (BEPS)

- India has ratified the Multilateral Convention to Implement Tax Treaty Related Measures to Prevent Base Erosion and Profit Shifting (multilateral instruments (MLI), which was signed by the Finance Minister in Paris in June, 2017 on behalf of India, along with representatives of more than 65 countries.

About MLI:

- It is a multilateral convention of the Organisation for Economic Co-operation and Development (OECD) to combat tax avoidance by multinational enterprises (MNEs) through prevention of Base Erosion and Profit Shifting (BEPS).

- The BEPS multilateral instrument was negotiated within the framework of the OECD G20 BEPS project and enables countries and jurisdictions to swiftly modify their bilateral tax treaties to implement some of the measures agreed.

- The BEPS multilateral instrument was adopted on 24 November 2016 and signed on 7 June 2017 by 67 jurisdictions for the first signing ceremony.

- As of July 2018, 83 jurisdictions have signed the BEPS multilateral instrument, covering more than 1,400 bilateral tax treaties.

- It entered into force on 1 July 2018, among the first jurisdictions that ratified it.

India and MLI:

- India was part of the Ad Hoc Group of more than 100 countries and jurisdictions from the G20, Organisation for Economic Co-operation and Development (OECD), and other interested countries, which worked on the finalising the text of the Multilateral Convention.

- The MLI will modify India’s tax treaties to curb revenue loss through treaty abuse and base erosion and profit shifting strategies by ensuring that profits are taxed where substantive economic activities generating the profits are carried out.

- The MLI will be applied alongside existing tax treaties, modifying their application in order to implement the BEPS measures.

- Out of 93 tax treaties notified by India, 22 countries have already ratified the MLI so far and the Double Taxation Avoidance Agreement (DTAA) with these countries will be modified by MLI.

- For the remaining countries with tax treaties with India, the MLI will come into force when they ratify it. The MLI will come into force for India from October 1, 2019.

What is Base Erosion and Profit Shifting (BEPS)?

- It refers to tax avoidance strategies that exploit gaps and mismatches in tax rules to artificially shift profits to low or no tax locations.

- BEPS is of major significance for developing countries due to their heavy reliance on corporate income tax, particularly from multinational enterprises (MNEs).

CENTRE EXPANDS TERMS OF REFERENCE OF DIRECT TAX LAW

27, Jun 2019

- The Central Board of Direct Taxes has expanded the terms of reference of the task force set up to come up with a new direct tax law.

- They include appropriate direct tax legislation keeping in view the direct tax litigation in other countries, international best standards, the economic needs of the country and other related issues.

- The new additions include the creation of a faceless and anonymized verification and security system, and the sharing of information between GST, customs and CBDT, and the Financial intelligence unit.

Data Localisation

19, Jun 2019

Context:

- RBI last year mandated companies to store their payments data “only in India” so that the regulator could have “unfettered supervisory access”.

- The RBI will examine concerns around its strict data localisation rules that require storing of customer data exclusively in India without creating mirror sites overseas.

What is Data Localisation:

- Data localisation laws refer to regulations that dictate how data on a nation’s citizens is collected, processed and stored inside the country.

Significance of Data Localisation:

- Data localisation is critical for law enforcement.

- Access to data by Indian law agencies, in case of a breach or threat, cannot be dependent on the whims and fancies, nor on lengthy legal processes of another nation that hosts data generated in India.

What India can do:

- It may not be wise for India to have the liberal rules as developed nation.

Legislation backup:

- Only Mandatory rule on data localisation in India is by the Reserve Bank of India for payment systems. Justice Sri krishna Committee report – to identify key data protection issues in India and recommend methods of addressing them”.

New Income Tax Rules With Revised Guidelines

18, Jun 2019

Why in News?

- Revised guidelines of Income Tax and to make strict decision against tax invaders new Income Tax guidelines has came into effect from, June 17, 2019.

- These revised guidelines issued by the Income Tax (IT) Department are for those who have made serious offences under black money and benami laws.

Highlights:

- The Central Board of Direct Taxes (CBDT), the apex direct tax policy making body, said in the new guidelines that any offence connected to undisclosed foreign bank account or assets in any manner cannot be compounded.

- India had introduced the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act in 2015 to curb unaccounted wealth kept abroad and to impose tax and penalty on such wealth.

- CBDT also said in the new guidelines that offences linked to any wrongdoing covered under the Benami Transactions (Prohibition) Act 1988 are also not compoundable.

- As per the new rules, a full tax rebate applies for individual taxpayers with a net annual income up to Rs 5 lakh. This means that the income limit eligible to avail tax rebate under Section 87A of the Income Tax Act has been increased from the earlier limit of Rs 3.5 lakh to Rs 5 lakh.

CBDT:

- The Central Board of Direct Taxes (CBDT) is a part of Department of Revenue in the Ministry of Finance.

- The CBDT provides inputs for policy and planning of direct taxes in India, and is also responsible for administration of direct tax laws through the IT Department.

- The CBDT is a Statutory Authority functioning under the Central Board of Revenue Act, 1963. The officials of the Board in their ex officio capacity also function as a division of the Ministry dealing with matters relating to levy and collection of direct taxes.

- The CBDT is headed by Chairman and also comprises six members, all of whom are ex officio Special Secretary to the Government of India.

FDI IN SERVICES SECTOR UP 37% IN 2018-19

06, Jun 2019

Why in News:

- Foreign direct investment (FDI) in the services sector grew 36.5% to $9.15 billion in 2018- 19, according to the Department for Promotion of Industry and Internal Trade (DPIIT).

Background:

- Services sector includes finance, banking, insurance, outsourcing, R&D, courier and analysis. The sector attracted FDI worth $6.7 billion in 2017-18.

- The sector accounts for about 18 per cent of the total FDI India received between April 2000 and March 2019. Raising FDI inflows in the services sector is vital as it contributes over 60% to the gross domestic product.

Foreign Direct Investment in India

- Foreign investments are crucial for India as the country needs around $1 trillion for overhauling its infrastructure sector such as ports, airports and highways to boost growth.

- A strong inflow of foreign investments helps improve the country’s balance of payments situation and strengthens the value of rupee against global currencies, especially the US dollar. However, the overall FDI inflows declined for the first time in the last six years in 2018-19, falling 1 per cent to $44.37 billion as foreign investments fell significantly in telecommunication and pharmaceutical sectors, official data showed. Recently the government has taken several measures like fixing timeliness for approvals and streamlining procedures to improve ease of doing business in the country and attract foreign investments.

GST BUOYANCY

04, May 2019

Why in News

- GST collections hit a record high, the next step should be to simplify the tax regime

Details:

- The GST inflows of ₹1,13,865 crore in April are the

- highest recorded since the tax regime was introduced in July 2017

- They represent an increase of over 10% compared to the same month a year ago

- GST revenues have crossed the ₹1 lakh crore mark Healthier GST collections, if sustained, will also mean less pressure on the Centre to cover its fiscal deficit. In the absence of more disaggregated data, it could be argued that tax rate cuts by the GST Council in December too may have spurred higher volumes for some goods and services. The rush to pay tax arrears at the end of the financial year may have been another seasonal factor contributing to better tax collection

GST

- It is a destination-based taxation system.

- It has been established by the 101st Constitutional Amendment Act.

- It is an indirect tax for the whole country on the lines of “One Nation One Tax” to make India a unified market. It is a single tax on supply of Goods and Services in its entire product cycle or life cycle i.e. from manufacturer to the consumer.

- There is a provision of GST Council to decide upon any matter related to GST whose chairman in the finance minister of India.

GST Council

- It is the 1st Federal Institution of India, as per the Finance minister. It will approve all decision related to taxation in the country.

- It consists of Centre, 29 states, Delhi and Puducherry.

- Centre has 1/3rd voting rights and states have 2/3rd voting rights. Decisions are taken after a majority in the council.

Centre should address States’ concern on GST transfers

29, Mar 2019

While the Goods and Services Tax (GST) Council was designed as a federal body between the States and the Centre, the complaint of the States is that the Centre is taking advantage of the arrangement and is delaying the dues to be paid to the States longer than is needed.

COOPERATIVE FEDERALISM

Though Indian states have achieved Political Integration in 1950’s with the integration of Princely states in Indian Union, economic Integration was still missing. Passing of GST is a shining example of cooperative federalism where States and Centre have ceded their power to tax and come up with a single tax system to realize the dream of one Economic India with ‘One Market’. Thus, GST once again has shown Unity in Diversity of Indian Society. However, Economic integration is still not achieved as Constitution needs some changes in this regard.

GST: a shining example of Cooperative federalism

In our Federal System both Centre and States have power to impose taxes. The division of such taxation powers is given in Union and State List under 7th Schedule. With the spirit of cooperative federalism, under GST, both Centre and States have given up taxation powers and as a product following taxes have been eliminated.

The Constitution of India has also been amended accordingly. This fundamental reordering of federal fiscal relations for the cause of common good shows the strength and resolve of the federal structure.

This convergence for the cause of larger public good has been made possible, initially due to the mechanism of the Empowered Committee of Ministers (EC) and later the GST Council. Under the GST regime, the Centre & States will act on the recommendations of the GST Council. GST Council comprises of the Union Finance Minister, Union Minister of State for Finance and all Finance Ministers of the States. 2/3rd of voting power is with the States and 1/3rd with the Centre which reflects the accommodative spirit of federalism.

Though the Constitution provides for decisions being taken by a 3/4th majority of members present and voting, all decisions till now (before july, 1, 2017) have been taken unanimously by consensus. The very fact that there has been no need to resort to voting to take any decisions taken till now in 18 meetings held so far reflects the spirit of “One Nation, One Aspiration, One Determination”. In this context it is important to note that credit for the new law does not go to one party or one government but it’s a shared legacy of all.

The participation of all States and Centre in the framing of GST laws has led to the following features in the GST Laws. These features signify spirit of cooperative federalism.

- Harmonisation of GST laws across the country: Even though Centre and each State legislature have passed their own GST Acts, they are all based on the Model GST law drafted jointly by the Centre & the States. Consequently, all the laws have virtually identical provisions.

- Common Definitions: There are common definitions in the CGST and SGST Act.

- Common Procedures / Formats:There are common procedures; common formats in all laws, even the sections and subsections in CGST Act and SGST Act are same. UTGST Act provides that most of the provisions in CGST Act, as stated in Section 21 shall apply to UTGST Act also.

- Common Compliance Mechanism: GSTN, a not-for-profit, non-government company promoted jointly by the Central and State Governments, is the common compliance portal and the taxpayers shall interface with all states as well as Centre through this portal.

Other significant areas, where such co-operation has been displayed by the Centre and States are as under: - Joint Capacity Building Efforts: Joint Capacity Building efforts by Centre as well as all the States are being organised wherein for the first time the training of officers of Centre and State is being conducted under the auspices of National Academy of Customs, Indirect Taxes and Narcotics (NACIN). NACIN has formed a Joint Coordination Committee in each State comprising of Centre, State and NACIN Officers for overseeing Capacity Building efforts.

- Joint Trade Awareness & Outreach Efforts: Centre along with the State Government Officials has been organising Joint Trade Awareness & Outreach programs wherein for the first time the Officers came together to create GST awareness amongst Trade and other stakeholders.

- Cross Empowerment of Officers of Centre as well as States:Though GST will be jointly administered by Centre and State, for ensuring ease of doing business, but the individual taxpayer will have a single interface with only one Tax Authority either Centre or State.

- Joint Implementation Committees: In order to ensure smooth rollout of GST, the GST Council has formed a three tier structure consisting of: the Office of the Revenue Secretary, GST Implementation Committee (GIC) and eight Standing Committees. In addition, eighteen Sectoral Groups representing various sectors of the economy have been set up. All these Committees viz. GST Implementation Committee (GIC), Standing Committees and Sectoral Groups have representation of Centre and State Officers in the spirit of cooperative federalism to ensure quick administrative decisions required before and after the rollout and ensure effective coordination for smooth implementation of GST.

Indeed, GST in India in its conception, enactment and implementation is an example of real ‘co-operative federalism’ at work, in tune with the unique character of India – ‘Unity in Diversity’.

Economic Integration

Under GST regime the entire country will become one market and it will be an economic integration of India. India would become one uniform market with seamless transfer of goods and services.

Indirect tax collection may fall short, says Garg

15, Mar 2019

The government is reasonably confident of meeting its direct tax collection target for the current financial year but the indirect tax collection may fall short.

The Rationale Behind:

- GST collections in February dropped to 97,247 crore in February from ₹1.02 lakh crore in the previous month.

- The government had lowered the GST collection target for current fiscal to ₹11.47 lakh crore in the revised estimates, from₹13.71 lakh crore budgeted initially.

- For the next fiscal 2019-20, the GST collection target had been budgeted at ₹13.71 lakh crore.

Classification of Taxes

What is a Tax?

- Taxes are generally an involuntary fee levied on individuals and corporations by the government in order to finance government activities. Taxes are essentially of quid pro quo in nature. It means a favour or advantage granted in return for something.

Direct Tax versus Indirect Tax

GST:

- Goods and Services Tax is a comprehensive indirect tax which is to be levied on the manufacture, sale and consumption of goods and services in India.

- GST eliminates the cascading effect of taxes because it is taxed at every point of business and the input credit is available in the value chain.

- France was the first country to introduce GST system in 1954.

- More than 140 countries have implemented the GST.

- The Genesis of GST occurred during the previous NDA Government under Atal Bihari Vajpayee Government when it set up the Asim Dasgupta committee to design a model for GST.

- The UPA Government took the matter further and announced in 2006 that this tax would be introduced from April 1, 2010. However, so far it was not introduced.

- All the GST bills including Constitution (101st Amendment) Act have been passed now and GST is set to come into force from July 1, 2017.

- GST would replace almost all vital indirect taxes and cess on Goods & services in the country.

GST can boost direct, Indirect Tax Collections

07, Jan 2019

In News:

- The fact that the government is increasingly dependent on tax revenue, especially indirect taxes, to meet its fiscal requirements is not a cause for worry, according to tax analysts, who say that the real benefits of the Goods and Services Tax (GST) have not yet taken effect.

- Once they do, government revenue from both direct and indirect taxes will grow significantly.

Explained:

- An analysis of the budget documents of the last five years has shown that the government’s dependence on tax revenue has steadily increased, with tax revenue making up a little more than 70% of its total receipts in 2018-19, up from 65% in 2014-15.

- Correspondingly, the share of revenue from non-tax sources (such as dividends from PSUs and the RBI) and capital receipts (such as disinvestment proceeds) has been declining. Within tax revenue, the analysis shows that the share of indirect tax has been growing over the years, increasing to nearly 50% in 2018-19 from a little less than 45% in 2014-15.

- This increased dependence on tax revenue to meet its fiscal needs has meant that the government has had to push quite hard to increase its tax base at both the direct and indirect tax levels.

- The view among tax analysts is that the government cannot take the risk of increasing tax rates, whether direct or indirect, for fear of a backlash from the public.

- So, the only option it has to boost tax revenues is to increase the tax base and stop evasion, both of which the government has been trying to do with measures like e-way bill, uniform taxation, analysing the business-wise monthly GST payments and ascertaining trends in State-wise movement of goods using the e-waybill data, operation clean money.

- The other trend the government would be banking on is that increased economic activity and a higher GDP growth rate will boost consumption and hence, indirect tax collections

- The indirect tax rate is fixed, so if there is price inflation, then the government receives a tax on that as well because product prices go up and so the tax component also goes up

- The second aspect is that when the GDP grows, consumption also grows, and so you get more indirect taxes from that.

- The worry for the government should be the fact that an increasing proportion of its indirect tax collections are coming from a single source — oil.

Non-Tax Revenue:

- The government has also been trying to improve its collections from other sources such as dividends from public sector companies and the Reserve Bank of India, and also through disinvestments.

- The analysis of budget data shows that PSU dividends as a proportion of non-tax revenue have been growing over the years, from 16% in 2014-15 to 21.4% in 2018-19. The government has reportedly been pressurizing the state-run oil companies to transfer larger dividends to the Centre every year.

- It is also reportedly asking the state-run oil companies to buy back shares, and is also pushing more PSUs to list on the stock exchanges.

- However, this is an untenable source of revenue for the government because they are based on finite resources.

- Notably, dividends from the RBI, as a proportion of non-tax revenue, have been falling.

- Non-tax revenues, if you look at the majority, they have come from auctioning spectrum licences and royalties from oil, etc., and also disinvestment.

Apparel Exporters Want Hike in Duty Drawback Rates

14, Dec 2018

In News

- Apparel exporters have appealed to the government to review the duty drawback rates announced recently for readymade garments

- The new rates announced by the government were 2.20 %-2.52 % percentage points short of what the council had sought.

Background:

- The drawback neutralizes customs duty and excise duty component on the inputs used for products exported. This is offered at fixed rates independent of tax levied on inputs.

- It is a relief by way of refund/ recoupment of custom and excise duties paid on inputs or raw materials and service tax paid on the input services used in the manufacture of export goods.

- Duty drawback provisions are given under section 74 and 75 of the Customs Act, 1962. Section 74 allows duty drawback on re-export of duty paid goods. Whereas section 75 allows drawback on imported goods used in the manufacture of export goods. In order to facilitate the drawback procedures, the Central Government is empowered to make rules

- The revised rates of duty drawback will help address the concerns of these export sectors and make India’s exports more competitive in global economy

- The higher duty drawback rates together with timely refunds will help exporters retain their competitiveness

Importance and Potential of Apparel Sector:

- The Indian textile industry is set for strong growth, buoyed by both strong domestic consumption as well as export demand

- The sector employs one of the vulnerable and underemployed gender of the India mainly women and it reinforces their financial freedom

- The fundamental strength of the textile industry in India is its strong production base of wide range of fibre/yarns from natural fibres like cotton, jute, silk & wool to synthetic /man-made fibres like polyester, viscose, nylon & acrylic

- The sector is expected to reach USD226 billion by FY2023

- Population is expected to reach to 1.34 billion by FY2019 and so the labor force & clothing needs

- Urbanization is expected to support higher growth due to change in fashion & trends

- The organized apparel segment is expected to grow at a Compound Annual Growth Rate of more than 13 per cent over a 10-year period

- India accounts 63 per cent of the market share of textiles and garments

- India accounts for about 14 per cent of the world’s production of textile fibres& yarns (largest producer of jute, 2ndlargest producer of silk and cotton; & 3rd largest in cellulosic fibre)

Benefits of Apparel Industry:

- Research and records have established the high potential of the apparel sector to create about 70 jobs for every crore rupee invested, much higher than the other manufacturing sectors.

- As high as Rs 26,000 crore are given out as salaries and wages every year by this industry.

- The most significant advantage lies in the high employability of women in this sector at every level- from a sewing machine operator to the CEO of a brand.

- It can greatly boost the export led growth of the Indian economy

WTO Conditions:

- The government also has to be careful now in giving duty drawback and ensure it is strictly according to inputs consumed as India is no more eligible to give export subsidies as per global trade rules as its per capita Gross National Income has crossed $1,000 for the third year in a row.

- The MEIS (Merchandise export incentive scheme) scheme, too, could be questioned by WTO members as it is an export subsidy and no more permitted.

CABINET CLEARS PROPOSAL TO MAKE GSTN 100 PER CENT GOVT- OWNED COMPANY

05, Sep 2018

Why in news?

- The Union Cabinet has cleared a proposal to convert the GST Network into a government- owned company, finance minister Arun Jaitley

GSTN:

- A few months ago, an in-principle decision was taken to make it a 100% government- owned entity. The GST Council has already approved the move. Now the cabinet has approved it.

- The restructured GSTN, with 100 per cent government ownership, shall have equity structure between the Centre (50 per cent) and the states (50 per cent).

- Currently, the Centre and the states together hold a 49% stake in the company, which provides the IT backbone to the indirect tax

- The remaining 51% is held by five private financial institutions – HDFC, HDFC Bank, ICICI, NSE Strategic Investment Co and LIC Housing Finance. The stake of the private companies will be acquired by the Centre and the state

- GSTN was incorporated as a private limited company on March 28, 2013, under the previous UPA government. It is a not-for-profit

- There had been criticism about allowing private companies to hold a majority stake in GSTN and demands to change its